Financial terms: Break even point

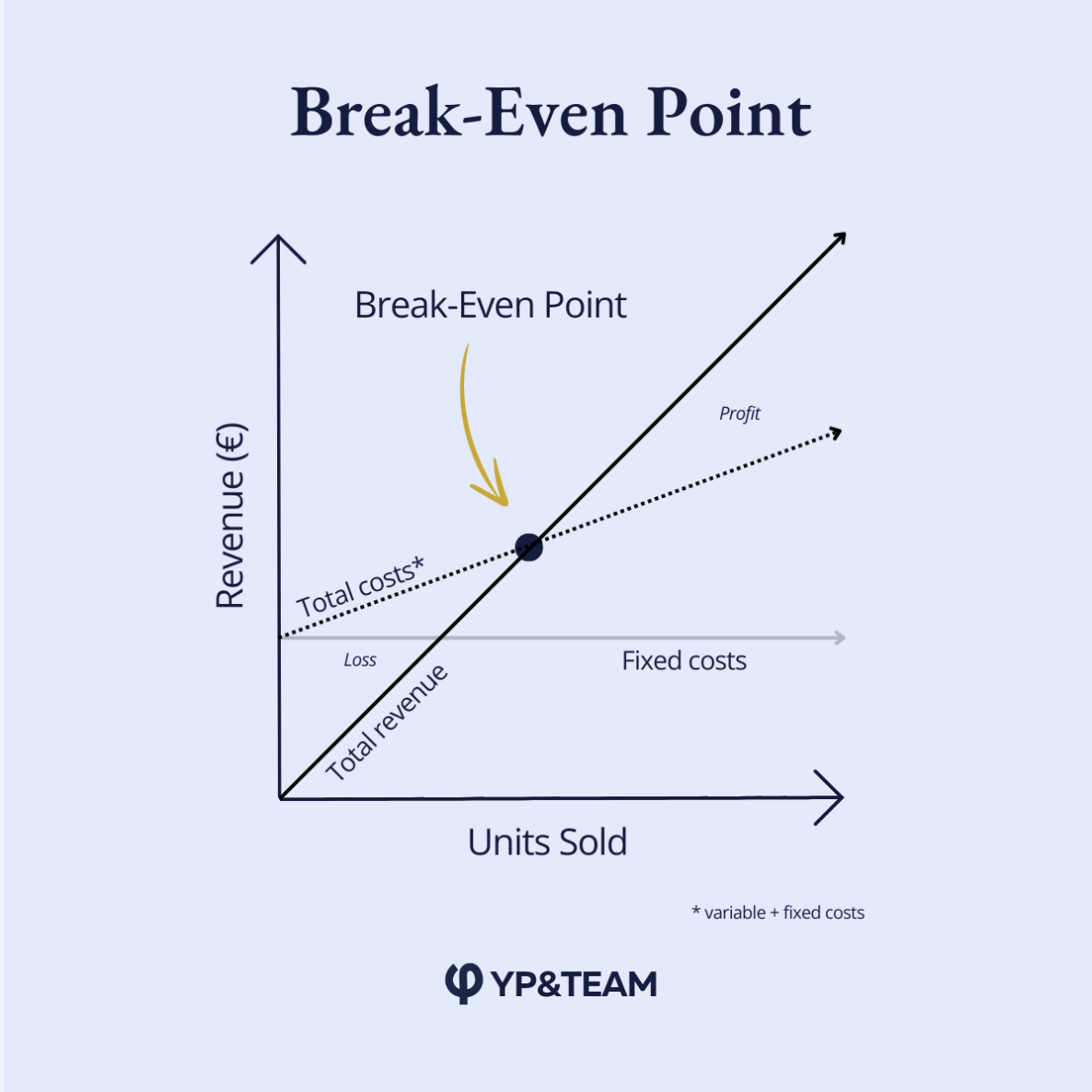

The break-even point is the critical milestone where your business transitions from covering startup debts to generating true profit. Whether you’re currently funding your launch or scaling operations, knowing your fixed costs and gross margin is the key to financial sustainability. Read our step-by-step guide to calculating your break-even point and moving your business into the "profit zone."

How to launch a collection: A Financial Planning Guide for The Fashion Designer

It all begins with an idea.